Cloud is where the money is, but can data centre operators take advantage?

Published:

Content Copyright © 2015 Bloor. All Rights Reserved.

Also posted on: IT Infrastructure

Revenue up 81% on the same quarter last year, $391 million profit and operating margins of 21.4%…AWS certainly seem to have developed a low cost, high value offering. We know that the major IT vendors and resellers are scrambling to deal with the implications of Cloud in general, and AWS in particular for their business models, but what about the co-location providers.

{kind=link}

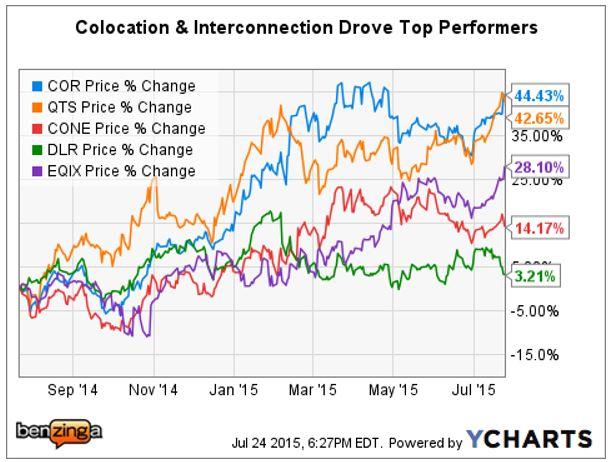

Q2 results from US data centre operator Coresite prompted an interesting review of stock price performance among Coresite’s Real Estate Investment Trust (REIT) peers, Equinix, Digital Realty, QTS Realty and CyrusOne. This highlights a fairly clear link between those companies whose data centres have high network density and a strong cloud eco-system with a higher performing stock price. Perhaps this highlights one of the key drivers of Digital Realty’s recent takeover of Telx.

Great, but if you try and jump on the cloud and interconnection bandwagon this won’t necessarily lead to greater revenues and greater margins. As the saying goes,” if you see a bandwagon it’s too late.” In the short to medium term, helping customers develop and deploy their hybrid cloud strategies by providing a world-class, interconnected data centre with a range of partners who can provide the Cloud and XaaS services required should enable you to stay away from the price fights in a vanilla co-location market. Being local, providing support “above and beyond” and building expertise in particular vertical markets will all help mitigate competitive pressures and help you find some defensible niches.

However, the long term end game is the complete retreat of businesses from owning and running their own servers. This ought to be good news for data centre operators but it isn’t necessarily the case. Making any sort of prediction in this industry is asking for trouble, but if you look at the progress that AWS, Microsoft, Google et al are making in terms of driving down the unit costs of computing whilst providing scale we could only dream about a few years ago, and the way they are doing it, then the likely outcome is a market dominated, like any utility, by a small number of very large players who can afford to build and maintain the infrastructure and the underpinning eco-system.

Traditional vendors like IBM, HP, Cisco, VMWare etc. will continue to claim that enterprises need the security, reliability and performance of their hybrid solutions and that the public cloud isn’t ready or right for them. Actually the biggest barrier to change and the wholesale adoption of public cloud is probably existing software. 25 years ago the mainframe was declared dead but it is still with us, albeit on life support while the software industry grapples with new applications and new development methodologies needed in the cloud world. It may well be another 25 years before we are anywhere close to that vision of a true computing utility, so there is no need to panic yet.

Ultimately though, doing nothing is not an option unless you have the lowest operating costs on the block. Just be aware that the big, game changing moves have already been taken in this market. You’ll be looking to make incremental improvements in shark infested waters. If you find blue water, it may well be in a pond rather than an ocean and it too will become shark infested and bloody quite quickly. You have to keep moving, or start the next bandwagon.

This post first appeared on the old Cassini Reviews website.